by Matthew Allen | Mar 30, 2025

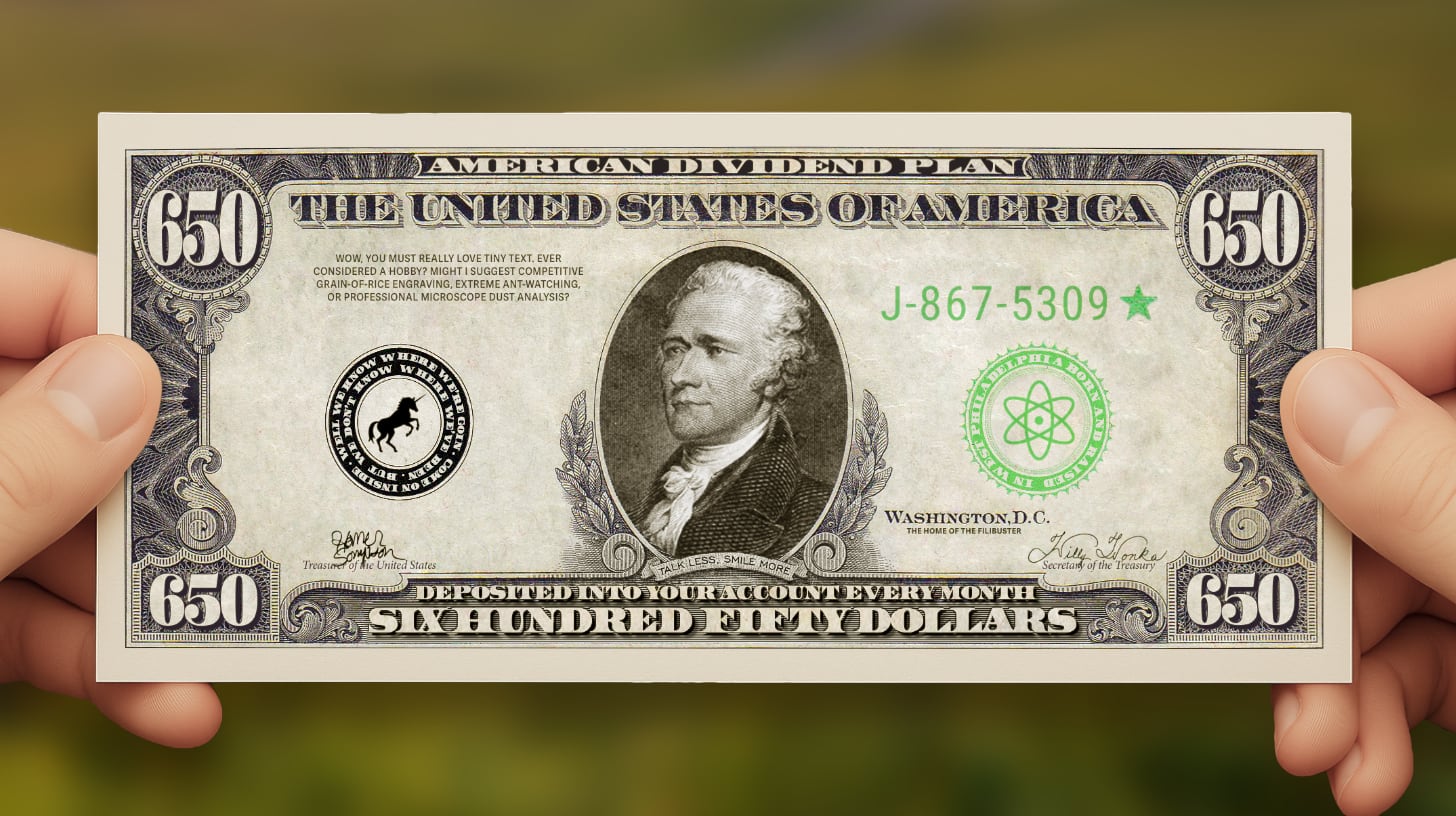

What if I told you every American adult could get $650 in their bank account every single month? I know, this probably sounds like one of those late-night infomercials where a guy with ridiculously white teeth promises a miracle cream that erases all wrinkles instantly, or a telemarketer telling you that you've been randomly selected to win a free vacation. But bear with me, because this is actually legit. Not some government handout, but your fair share of America’s prosperity. And what if I told we could fund this without adding a penny to the national debt.

I should clarify that I’m not technically a Nobel Prize-winning economist. Although I did once try to explain inflation to my five-year-old using only dinosaur figurines. I once thought a bear market meant something was happening at the zoo, and that a “hedge fund” was just a fancy savings account for landscaping expenses. But I do know suffering when I see it, and working class Americans have been getting pummeled for a long time now. And I'm tired of watching working people struggle while billionaires build rockets for their phallic joyrides.

So, buckle up for a plan that could genuinely change your life.

Welcome to the American Dividend, where we all get a slice of the American pie we’ve been baking together.

So what exactly is this American Dividend? It’s pretty simple, actually. Every American adult gets $650 deposited directly into their account each month. That’s it. No complicated forms, no means testing, no bureaucrats deciding if you qualify. If you’re a US citizen over 18, you get the dividend.

Let’s break down what that means. That’s $7,800 a year for individuals, $15,600 for couples. If you’re a household with two adults, that’s $1,300 hitting your bank account every month. Not just pocket change.

Now, I know what you’re probably thinking. “This sounds like some kind of handout.” But it’s not. I prefer to think of it as a dividend: your share as a partial owner of the greatest economic engine in human history: America.

Think about it. When you own stock in a company, you get dividends. Well, we all contribute to America’s success: through our work, our taxes, our communities. So why shouldn’t we all benefit from that success? For too long, the gains have flowed almost entirely to the top. The American Dividend just makes sure everyone gets a fair share.

And let me tell you, this would be life-changing for the bottom 50% of Americans. If you’re living paycheck to paycheck, an extra $650 a month is the difference between constant stress and actually being able to breathe. It’s the difference between one emergency away from disaster and having a little cushion. For the middle class, it’s money for home repairs, college savings, or maybe (imagine this) an actual vacation.

Remember those RUBI voters we talked about in Episode 1? The ones who are Radically Uninformed and Blindingly Inattentive because they’re too busy trying to survive? This is exactly the kind of straightforward policy that would get their attention. No PowerPoint needed. Just: “You get $650 a month. Period.” That’s something anyone can understand, no matter how stressed or overwhelmed they might be.

But, I can hear the questions already. “Why not just raise the minimum wage? Why not better welfare programs? Why not just create more jobs?”

All fair questions. Let’s take them one by one.

Look, I’m not against higher minimum wages. But they have limits. For starters, they only help people with jobs. If you’re a stay-at-home parent, student, disabled or retired person, or someone starting a business, minimum wage does nothing for you. And let’s be honest: raise it too high too fast, and we run into unintended problems.

Small businesses that operate on thin margins get squeezed. The local diner or hardware store might have to cut staff, reduce hours, or even close up shop. The cruel irony? We end up hurting some of the very people we’re trying to help. Some workers get better pay, while others lose their jobs entirely. This is not exactly the win-win we’re looking for.

Plus, minimum wage doesn’t address automation replacing jobs, or the fact that $15 an hour means something completely different in San Francisco than it does in rural Kentucky.

Again, I’m all for improving our safety net. But have you seen the current system? It’s a bureaucratic maze with different applications, different rules, and benefit cliffs that can actually punish people for earning more. It’s stigmatized, often dehumanizing, and expensive to administer. And it’s way too easy for politicians to cut programs serving people who don’t have lobbyists.

Yes, please! But jobs alone aren’t enough. First off, not all valuable work comes with a paycheck. Raising kids, caring for elderly parents, volunteering in your community: this labor (often done by women) props up our entire economy but gets zero compensation.

Then there’s the fact that economic disruptions happen. Pandemics, recessions, technological change. You can have the perfect job one day and be unemployed the next. And some regions struggle to attract employers no matter what incentives we throw at them.

This is where the American Dividend shines. It’s universal: covering everyone regardless of work status. It’s simple: no complex eligibility rules. It’s empowering: you decide what you need, not some bureaucrat. It moves with you anywhere in America and continues during economic downturns when you need it most.

Unlike minimum wage hikes, the American Dividend boosts consumer spending without forcing businesses to cut jobs. In fact, it creates customers for local businesses because people have money to spend.

Look, I’m not against other policies. Raise the minimum wage within reason? Sure. Better healthcare? Absolutely! But the American Dividend does something nothing else can: it gives people the freedom to solve their own unique problems, whether that’s starting a business, going back to school, leaving an abusive relationship, or just having enough breathing room to stop working three jobs.

Money might not solve everything, but lack of money sure creates a lot of problems.

Alright, let’s talk about the elephant in the room: How do we pay for this?

I want to be totally transparent about the math here, because this has to work financially or it’s just a nice theory. So here’s the bulletproof funding plan:

We establish a 10% Value-Added Tax, often referred to as a “VAT tax”. Now before your eyes glaze over at the tax talk, hang in there, because this is different from the taxes you’re used to.

(And by the way, I’m gonna keep saying “VAT tax” which is totally redundant since VAT already stands for Value Added Tax. It’s like when I say “PIN number” or “PDF format” or my personal favorite, “please RSVP.” My editor keeps highlighting this in red, but honestly, “VAT” alone just sounds weird hanging out there by itself. It needs that little “tax” buddy to sound complete. I’m fully aware this makes me sound like the kind of person who says “ATM machine” while ordering “chai tea,” but sometimes being technically wrong just sounds so right. Grammar nerds, I see you cringing, but I stand defiant.)

A VAT tax is what is known as a “consumption tax”: it applies to goods and services when value is added at each stage of production or distribution. I know that sounds complicated, but it’s actually used in 160 countries around the world. America is one of the only developed nations without one.

A VAT tax is better than other options because it’s much harder to dodge than an income tax. Even if you’re a corporation with fancy lawyers finding loopholes in the tax code, you can’t escape a VAT tax. It’s more stable than wealth taxes, which can be tricky to implement. And it ensures that companies like Amazon and Google, which are masters at avoiding corporate taxes, finally pay their fair share.

But what exactly is “value-added”? Let me break it down with a simple example. Imagine a bakery. A farmer sells wheat to a mill for $1, and there’s a 10 cent VAT tax. The mill grinds it into flour and sells it to a baker for $3, with a 30 cent VAT tax (but they get credit for the 10 cents already paid). The baker makes bread and sells it for $6, with a 60 cent VAT tax (minus the 30 cents already paid). At each step, the VAT tax only applies to the new value created.

Now, I know what you’re thinking: “Won’t this just make everything more expensive?” That’s why we’re designing this with multiple tiers:

This tiered approach ensures the system is fair. We’re not taxing people’s groceries or medicine, but that $5,000 designer watch? Yeah, that’ll have a bit extra on it.

When all the math is done, a 10% VAT tax with these tiers would generate approximately $2.1 trillion annually based on conservative estimates of US consumption patterns. This is enough to fund the full $650 monthly dividend for all American adults, cover administrative costs (about 2% of the program), and maintain a stability fund to ensure consistent payments even during economic downturns.

This isn’t magical thinking or money printing. It’s a carefully balanced system that works in almost every other developed country in the world. And it’s about time it worked for us too.

I understand some skepticism here. Big ideas should be tested before going nationwide. So here’s how we make this work in the real world:

We’ll select diverse regions across America - a mix of urban, rural, struggling, and thriving communities - to receive the full $650 monthly dividend. These pilots would be directly funded by Congress, no VAT tax yet. We’ll closely study the effects on:

This gives us actual data instead of theoretical projections.

Once we see the dividend works in our pilot regions, we implement it nationwide along with a gradual VAT tax introduction:

Complete the transition to the full 10% VAT tax and $650 monthly dividend, with adjustments based on what we’ve learned from the earlier phases.

This measured approach ensures we’re not just implementing a theory but building a program proven to work in American communities.

Think of it like introducing your picky five-year-old to vegetables. You don’t start with Brussels sprouts casserole. You ease in with a carrot stick here, a piece of broccoli there, and before you know it, they’re eating kale smoothies. Okay, maybe not kale smoothies, but you get the idea.

Let’s tackle one of the biggest concerns head-on: What happens when millions of Americans suddenly have more money for housing in areas already facing housing shortages?

This is a legitimate question that requires serious attention. That’s why the American Dividend must be paired with a comprehensive 5-point housing strategy:

By proactively addressing housing supply alongside the dividend, we ensure the increased purchasing power helps people secure better housing rather than just driving up prices in supply-constrained markets.

As for general inflation, the data from cash transfer programs worldwide consistently shows minimal inflationary effects when structured properly. By funding the dividend through a VAT tax rather than deficit spending or money creation, we’re redistributing existing purchasing power rather than creating new money.

Now, I know what’s coming. The second anyone proposes something like this, the critics swoop in with their talking points. So let me get ahead of the usual suspects.

This would be true if we just slapped a flat VAT tax on everything and called it a day. But we’re not doing that. Remember, essentials like groceries and medicine aren’t taxed at all. And here’s the kicker: we’re including a rebate system for low-income households. If you make less than $25,000 a year, you’ll get a rebate that offsets the VAT tax you pay on taxable purchases. So the system actually ends up being progressive, not regressive.

Really? Giving every American a share of our collective prosperity is socialism? Last I checked, dividends are a feature of capitalism, not socialism. This isn’t the government taking over industries. It’s simply ensuring that the benefits of our economy don’t just flow to the top. It’s capitalism where everyone gets to participate, not just those born with advantages or lucky enough to be in the right place at the right time.

That’s pretty damn condescending. The whole “poor people can’t be trusted with money” argument is just snobbery dressed up as concern. And let’s be real, if we’re talking about questionable spending habits, none of us should throw stones. We all buy stuff we don’t need, order takeout when there’s food at home, and occasionally wake up wondering why we thought we needed an air fryer at 1 AM.

Freedom means other people get to make decisions you might not agree with, including how they spend their money. If you’re comfortable with a billionaire buying yet another yacht, but worried about a struggling parent splurging on a six-pack, maybe examine where that concern is really coming from.

Besides, the research consistently shows that when people get direct cash assistance, they spend it on boring, responsible stuff like housing, food, education, and getting out of debt. Turns out people actually know what they need better than some stranger with a clipboard and a lot of assumptions.

This isn’t about printing new money, which can cause inflation. It’s about redistributing existing money through a VAT tax system. And actually, the VAT tax itself helps control inflation by removing some purchasing power even as the dividend adds it back. Countries with VAT taxes don’t see higher inflation than the US; in fact, many have lower inflation. Plus, our targeted housing policies will address the sector most vulnerable to inflationary pressure.

Look, I get it. Big ideas make people nervous. But what should make us more nervous is continuing down our current path where millions of Americans work themselves to exhaustion and still can’t make ends meet. That’s the real disaster, and the American Dividend is our way out.

Let me be crystal clear about something important: The American Dividend is designed to complement existing supports for people with specialized needs, not replace them.

If you’re receiving disability benefits, medical assistance, or other targeted support for specific needs, the dividend would be additional help, not a replacement. These specialized programs exist because some people have greater needs, and that won’t change.

The dividend is a floor, not a ceiling. It’s the baseline economic security everyone deserves, regardless of their situation, while maintaining additional support for those who need it.

This approach ensures no one falls through the cracks while extending economic dignity to everyone.

Let’s break down the refined numbers, because I want you to see that this isn’t just some feel-good fantasy. The math actually works.

The total annual cost of giving every adult American $650 per month comes to about $2 trillion. That’s based on approximately 258 million adults in the US. Big number, right? But here’s where it gets interesting.

Our 10% VAT tax with the tiered structure would generate approximately $2.1 trillion annually. That covers the full cost with about $90 billion to spare. We’ll use about $40 billion of that for administration costs, which is actually pretty efficient at just 2% of program costs. Compare that to some existing programs where administration eats up 7% or more of the budget.

That still leaves us with a $50 billion buffer for economic fluctuations or unexpected needs. Again, this isn’t deficit spending or printing money. It’s fully funded through the VAT tax.

Now, how does this compare to other major government programs? Social Security costs about $1.3 trillion annually. Medicare and Medicaid combined are around $1.5 trillion. The military budget is over $800 billion. So yes, the American Dividend would be a major program. But it’s within the scale of what we already manage, and it would benefit every single American adult directly.

Here’s another way to think about it: The US economy is around $26 trillion. We’re talking about redirecting about 8% of that through a VAT tax to ensure everyone gets a baseline share of our collective prosperity. When you consider that the top 1% of Americans now own more wealth than the bottom 90% combined, this modest redistribution starts to look not just reasonable, but necessary.

And unlike many government programs, the American Dividend doesn’t create a massive bureaucracy. The money goes directly from the Treasury to your bank account. No caseworkers deciding if you qualify. No monthly reporting requirements. No surprise audits or benefit cliffs.

Just a simple acknowledgment that in the richest country in the world, everyone deserves a floor beneath their feet.

Now, there’s a problem with one-size-fits-all approaches that we need to address head-on. Let’s be real: $650 means completely different things depending on where you live.

In San Francisco, $650 might cover… what? Half your utility bill? A fraction of your rent? But in rural Kentucky or Mississippi, that same $650 could be transformative, potentially covering housing costs entirely.

This geographical inequality is one of America’s most persistent problems. Some regions have been booming for decades while others have been left in the dust. The American Dividend can help address this disparity, but we need to be smart about it.

Here’s how we make it work for everyone, everywhere:

First, we’ll implement a reduced 7% VAT tax in economically distressed counties instead of the standard 10%. We’re talking about counties with persistent poverty (where over 20% of people have lived in poverty for three decades or more), or counties that have lost more than 10% of their jobs in the past decade. This means people in struggling regions pay less in consumption taxes, which matters a lot when incomes are already lower.

Second, residents in these same economically distressed counties will receive a boosted dividend of $715 per month instead of $650. That extra $65 might not sound like much, but it’s $780 more per year, enough to make a real difference in areas where costs are lower but opportunities are scarcer.

Third, we’ll allocate a portion of that buffer we talked about for targeted infrastructure investments in these struggling counties. This means expanding broadband access in rural areas, improving public transit in urban food deserts, and creating job training programs where industries have disappeared.

This regional adjustment approach does something powerful: it creates incentives for economic activity to spread more evenly across America. Right now, wealth and opportunity are hyper-concentrated in a handful of urban centers. The American Dividend, with these regional adjustments, would help revitalize forgotten communities while giving people more freedom to stay where they are or move where they want.

Think about what this means for small towns across America that have been hollowed out as jobs moved overseas or to big cities. An extra $715 a month for every adult means new customers for local businesses. It means young people might be able to afford to stay instead of having to leave for opportunities elsewhere. It means communities can start rebuilding what they’ve lost.

This isn’t just economically smart, it’s about healing America’s geographic divide and making sure no region is left behind in our shared prosperity.

Numbers are one thing, but let’s talk about what the American Dividend would actually mean for real people. Because at the end of the day, that’s what matters.

Let’s look at three different household situations: a low-income essential worker, a middle-class family with unexpected medical costs, and a high-earning professional couple.

That’s the thing about the American Dividend. It’s not just about the direct cash benefit. It’s about creating a healthier society where everyone has at least some economic breathing room. And that makes life better for all of us, even those at the top.

Alright, so I hope I’ve convinced you that the American Dividend is a good idea. But how do we actually make it happen? Because let’s be honest: rolling out a program that touches every adult in America isn’t exactly like setting up a lemonade stand.

We need a phase-in period. You can’t just flip a switch on something this big. As outlined earlier, we’d start with regional pilots to prove the concept, then implement it gradually nationwide over three years. The VAT tax would start at 5% with a $325 monthly dividend, then scale up to the full 10% VAT tax and $650 dividend.

This gives businesses time to adapt their systems for the VAT tax. It gives people time to adjust their spending habits. And it gives the government time to work out any kinks in the distribution system.

Speaking of distribution, the beauty of the American Dividend is that we can use existing infrastructure. We don’t need to create some massive new bureaucracy. The IRS and Treasury already have systems for sending money to most Americans through tax refunds and Social Security. We’d leverage those existing systems while creating simple options for those who don’t have bank accounts or aren’t in the system, like reloadable debit cards or accounts at local post offices.

What about verification? Again, we keep it simple. Social Security numbers already tell us who’s an adult citizen. For the tiny fraction of people with unusual situations, we create straightforward processes to verify identity. This isn’t about making people jump through hoops. It’s about ensuring everyone gets their dividend with minimal hassle.

We need to handle special cases, of course. What happens when someone turns 18? They get automatically enrolled and start receiving their dividend the following month. New citizens? Same deal: once citizenship is granted, the dividend begins. People in prison? Their dividend gets held in an account and released to them upon completion of their sentence, giving them a financial cushion for re-entry into society.

On the technology side, we need a secure, user-friendly system that works for everyone from tech-savvy millennials to seniors who’ve never used a smartphone. The good news is we’re not reinventing the wheel here. The basic technology for direct deposits and electronic transfers already exists. We just need to make it more accessible and reliable.

The key to making all this work is keeping it simple from the user’s perspective. No complicated applications. No monthly reporting requirements. No surprise eligibility reviews. Just a straightforward system that treats people with dignity and respect.

Because at the end of the day, that’s what the American Dividend is all about: recognizing the inherent value of every person in our society and ensuring everyone has a baseline level of economic security.

Now let’s talk about something really exciting: what happens when you suddenly have millions of Americans with more money in their pockets. Because the American Dividend isn’t just about helping individuals, it’s about transforming our economy from the ground up.

First, we get a local business boom. When people have more money, they spend it, and they tend to spend it close to home. That coffee shop you love? They’ll have more customers. The hardware store down the street? Busier than ever. The family restaurant that’s been struggling? They might actually make it. This isn’t trickle-down economics. It’s what I call “ripple-out economics”: prosperity that starts with regular people and amplifies throughout the community.

Next, we see an entrepreneurship explosion. Ask people why they don’t start that business they’ve been dreaming about, and the answer is usually the same: “I can’t afford to take the risk.” The American Dividend changes that equation. When you have $650 a month guaranteed, taking a chance on a new venture becomes a lot less scary. That food truck idea? That Etsy shop? That landscaping business? Suddenly, they’re all within reach. We could unleash a wave of innovation and creativity unlike anything we’ve seen in generations.

Third, we give workers more power. Right now, millions of Americans are stuck in jobs they hate because they can’t afford to miss a single paycheck. The American Dividend gives workers breathing room to say “no” to abusive bosses, dangerous conditions, or exploitative pay. It doesn’t mean people will stop working. Studies consistently show that recipients in programs like this continue to work. But it does mean they can be more selective about where and how they work. And that forces employers to treat workers better and offer more competitive wages.

Fourth, we reduce all kinds of social costs. When people have their basic needs met, we see reductions in emergency room visits, homelessness, domestic violence, and even crime. Think about how much we spend dealing with the fallout from poverty, from policing to emergency services to incarceration. The American Dividend addresses these issues at their root, potentially saving billions in social costs that don’t show up in the direct program calculations.

Finally, we create what I call the “mobility multiplier.” Right now, many Americans are trapped in declining areas because they can’t afford to move where the jobs are. Others are forced to leave communities they love because there’s no way to make a living there. The American Dividend gives people the freedom to live where they want, whether that’s staying in their hometown to help revitalize it or moving to a new city for better opportunities. This mobility is good for the economy as a whole, ensuring talent can flow where it’s needed.

When you add all these effects together, what do you get? A more dynamic, more equitable, more resilient economy. One where prosperity isn’t just concentrated at the top, but spread throughout society. One where taking risks and trying new things isn’t just for those with rich parents or venture capital connections. One where every community has a chance to thrive.

And that’s an economy worth building.

So here we are. We’ve got this idea that could genuinely transform the country. But ideas without action are just daydreams. How do we actually make the American Dividend a reality?

First, we need to recognize something important: this plan has potential for bipartisan appeal. It’s not about growing government bureaucracy. In fact, it’s one of the most streamlined approaches to addressing poverty and economic insecurity ever proposed.

For conservatives, the selling points are clear: It’s not means-tested. It doesn’t create new bureaucracy. It treats everyone equally. It promotes freedom and individual choice. It supports family formation and stability. It revitalizes struggling communities without government micromanagement. And let’s not forget, it was conservative economist Milton Friedman who first proposed a version of this idea decades ago.

For progressives, the benefits are equally compelling: It provides immediate relief to those struggling most. It reduces poverty and inequality. It values unpaid care work. It gives workers more bargaining power. It creates a universal floor that can’t be easily dismantled. And it acknowledges our collective responsibility to ensure no one falls through the cracks.

The messaging playbook is straightforward:

Building the coalition to support this will require unlikely allies coming together. Imagine tech entrepreneurs alongside labor unions. Libertarians alongside social justice advocates. Rural community leaders alongside urban reformers. Religious organizations alongside secular humanists.

This idea isn’t as far-fetched as it sounds. There’s already growing support for this kind of Universal Basic Income (UBI) program across the political spectrum. Former presidential candidate Andrew Yang built a movement around a similar concept. Alaska’s dividend program remains wildly popular among Republicans and Democrats alike. Pilots and experiments are popping up in cities and states across the country.

The legislative path won’t be easy, but it’s not impossible. It starts with building grassroots support and demonstrating the idea’s viability through those regional pilots I mentioned earlier. We show it works. We build momentum. We elect representatives who support it. And eventually, we reach the critical mass needed for national implementation.

Will it happen overnight? Of course not. Major policy shifts rarely do. But the American Dividend is the kind of big idea that can capture imaginations and unite people across traditional dividing lines. And in our hyperpolarized political environment, that alone makes it worth fighting for.

Because at the end of the day, this isn’t about left versus right. It’s about whether we want to continue with a system that’s clearly failing millions of Americans, or whether we’re ready to try something bold that might actually solve our problems.

I know which side I’m on. How about you?

Look, I get it. This might sound too good to be true. A check for $650 showing up in your account every month? A better economic system that works for everyone, not just those at the top? It feels like fantasy in a world where we’ve been told over and over that nothing can really change.

But the math checks out. The economics makes sense. And most importantly, it would actually help real people living real lives.

We’ve tried trickle-down economics for decades, and what has it gotten us? The largest wealth gap since the 1920s. Stagnant wages for most Americans despite skyrocketing productivity. Millions of people working multiple jobs and still struggling to make ends meet.

We’ve tried complicated safety net programs, each with their own eligibility requirements, paperwork burdens, and benefit cliffs. What has that gotten us? A system so complex that many people who qualify don’t even access the benefits they’re entitled to. A system that often treats people with suspicion rather than dignity.

Maybe it’s time we try something radically simple: just making sure everyone gets their fair share of America’s prosperity.

Remember in our earlier episodes when we talked about finding a celebrity candidate who could break through to those RUBI voters, folks too stressed and overwhelmed to engage with complex policy debates? Imagine that candidate standing on stage saying, “Every American adult will get $650 a month, period.” That’s the kind of clear, powerful message that cuts through the noise and speaks directly to people’s lives.

And pair that with our “Build a Longer Table” tax plan from episode 4, where we eliminate taxes entirely for those making under $50,000 while asking the wealthiest to contribute more. Suddenly, you’ve got a comprehensive economic vision: zero taxes for those struggling most, a monthly dividend for everyone, and a more balanced system where prosperity is shared, not hoarded.

This isn’t just a collection of policies. It’s a new social contract. One that says if you’re part of this American project, you deserve both the freedom from financial desperation and the opportunity to build something better.

The American Dividend isn’t just another policy proposal. It’s a reimagining of what our economy could be, one where everyone has a floor beneath which they cannot fall, and a stake in our collective success.

When everyone has enough to meet their basic needs, we all benefit. Crime goes down. Health improves. Innovation flourishes. Communities strengthen. The constant stress that wears down so many Americans? It eases, replaced by the freedom to plan, to dream, to contribute in meaningful ways.

And just imagine explaining this to your politically opposite uncle at Thanksgiving. For once, you might actually agree on something before the pumpkin pie arrives. That alone might be worth the entire $2 trillion investment.

This is the American Dividend. Together with our other proposals, it forms a blueprint for an America that works for everyone. Because a country isn’t truly great unless it’s great for everyone.

The question isn’t whether we can afford to do this. The question is whether we can afford not to.

Get episode updates via email

We'll never share your email, period. We only hit your inbox to announce a new episode, and if you ever want out, unsubscribing is one click. Easy peasy.