by Matthew Allen | Mar 18, 2025

Here’s a quote you might’ve heard that’s at the heart of this idea:

“When you have more than you need, build a longer table, not a higher fence.”

It’s such a great quote, even the Bible echoes it. Check this out:

Now, I’m not really religious, but damn, Jesus was out there speaking truth to power. Can we all just agree that life is better when we’re sitting together at a longer table, and everyone gets a plate?

Look, I’m not a tax wizard. I’m not some genius economist, financial guru, or even someone who can confidently calculate a tip without my phone. I’m just a dad trying to make sense of the chaos out there. Sure, my family is doing okay, but holy hell, have you seen how rough it is for so many others? And it just feels like the political establishment doesn’t give a flying crap.

If you’ve read my blog about RUBIs and why they voted for Trump, you’ll probably remember: a huge chunk of Trump voters backed him because they believe he’ll put more cash in their pockets. Are they right? Probably not. But hey, desperate people make desperate choices.

Fair warning, I’m about to simplify a lot of this tax stuff. If you’re an expert, you might want to prepare for some a little eye-rolling. For the rest of you, stay open-minded. You might walk away with some new found insight. Or at least a laugh or two.

Here’s where it gets messy:

Interesting sidenote: Albert Einstein — yes, the Einstein — once said, “The hardest thing in the world to understand is the income tax.” If the guy who redefined space and time couldn’t wrap his head around taxes, we’re in pretty good company.

Imagine a better tax system that:

Is it really so wild to ask the people with the most money to chip in a little, to help those people just trying to survive? That’s what “building a longer table” is all about, giving everyone a chance to sit down and eat, without a fence in sight.

Alright, buckle up, because before we can start building that longer table, we need to take a quick detour into tax history. I know, it sounds about as exciting as reading the terms and conditions on a software update, but don’t worry. This ride comes with a few laughs along the way. Plus, by the end, you’ll see why the whole “build a longer table” idea actually makes a lot of sense. Let’s dive in.

Believe it or not, tax history is something people actually study. On purpose. ¯\_(ツ)_/¯

Once upon a time, the wealthiest Americans handed over a bigger slice of the pie. Here’s a quick, mildly entertaining rundown of how tax rates have shifted, because who doesn’t love a good tax story?

Back when these top tax rates were higher, life for the average American was pretty solid. The economy was chugging along, and the middle class was thriving. Uncle Sam was asking the wealthy to chip in a lot more, which helped pay for things like schools, highways, and those shiny post-war suburbs.

Income inequality (the gap between rich and poor) was way lower than today. Look, it wasn’t perfect, there were still plenty of problems, especially for marginalized communities. But overall, folks were buying homes, building nest eggs, and taking actual vacations without maxing out their credit cards. Turns out, when the wealthy pay more, everybody else gets a bit more of the pie. Who knew?

In 1986, tax rates for the wealthiest were slashed to 28%, in the name of this clever new concept called “Trickle Down Economics”. Get this: the idea was to have the wealthy pay way less in taxes and that would somehow mean that the rest of us would benefit. Yeah, bonkers.

Imagine somebody wealthy saying: “So all this money I used to contribute? Yeah, no. I’m going to keep all that now, and, trust me, this will actually help you more in the end.”

See how clever that is?

Interesting sidenote: Long before Reagan came along with his clever “trickle down” idea, this economic strategy had a much more honest nickname: “The Horse and Sparrow Theory.” The idea was that if you feed a horse enough oats, eventually some will be crapped out for the sparrows to pick through. In this metaphor, the wealthy are the horse, and us poor folk are the sparrows. We’re just birds eating leftover horseshit from the rich. At least they were honest about it back then. Mmmm good!

This was a massive change. For over 70 years, the wealthiest had been paying their fair share of taxes. Sure, there were issues with the tax code. But at the heart of this tax reform bill was a huge promise that if we just reduced taxes on the wealthy, we’d all benefit.

That is a whopper of a promise. And it basically boils down to “trust us”.

And just to be clear, this tax reform bill had broad bi-partisan support. Even Democrats were largely on-board with it. So while the idea of trickle down economics is typically credited to Reagan, Democrats were right in there with him, pushing this massive change.

Since then, tax rates for the wealthy have hovered between 35% and 39%. While these rates are somewhat higher than 28%, they have also come with new loopholes and deductions that favor the top earners. One of the original theories of the 1986 tax reform bill was that it would be “fairer” because it would eliminate all these loopholes.

Funny how those little buggers just sneak back in there.

So, since those top tax rates were cut in 1986 with that whopper promise of “trust us”, it hasn’t all been sunshine and bacon the way they said it would be. Instead, three things have happened:

Bottom line: trickle down economics simply hasn’t worked.

In reality it has turned out to be a cruel joke, and one that we’re still paying for. Some might generously call it a “misguided theory”, but I call it a scam. They knew exactly what they were doing. And the data over the last 30 years is conclusive: the trickle down concept is an economic failure for average Americans.

Inequality between rich and poor has increased, massively. And the impact on economic growth: minimal.

For the wealthiest among us? Well, it’s clear they’ve made out quite nicely. But it’s time we got back on track with a tax system that is fair and balanced. (No pun intended.)

Look, this isn’t about villains or heroes, it’s about leveling the playing field. We’re not here to demonize the wealthy; that misses the point. Hell, some of my best friends are wealthy, as the saying goes. Instead, I choose to believe that most of the wealthiest folks in our country are reasonable and are smart enough to realize that a broader prosperity is good for everyone, even them.

Skeptical? Here’s why I say that. In 2024, research firm YouGov polled millionaires in the US. Turns out, a majority of them are totally on board with paying more in taxes. I know, right? I’m just as floored as you are.

Here’s what they found:

So just to make sure this point hits home: Even the majority of wealthy folks in this country agree the wealthy should pay more taxes. They seem to have their hearts and heads in the right place. Refreshing, isn’t it?

However, a small minority of wealthy individuals don’t agree. Let’s call these folks the Hoarders. Even kindergartners know how to share crayons, but these Hoarders think sharing is something only suckers do. They clutch their loopholes like precious treasure, avoiding taxes with the zeal of a dragon guarding its hoard.

And that’s just sad. It’s like: “Who hurt you?”

And let’s be real, these are probably the people Jesus had in mind when he mentioned “selfish pricks” back in Matthew 25. (Again, paraphrasing.)

If the majority of wealthy people can see the value in creating a fairer tax system, maybe there’s hope for all of us. It’s a reminder that helping others, whether through taxes, donations, or good old fashioned kindness, isn’t just about following the Golden Rule. It’s about making life better for everyone, even the wealthy.

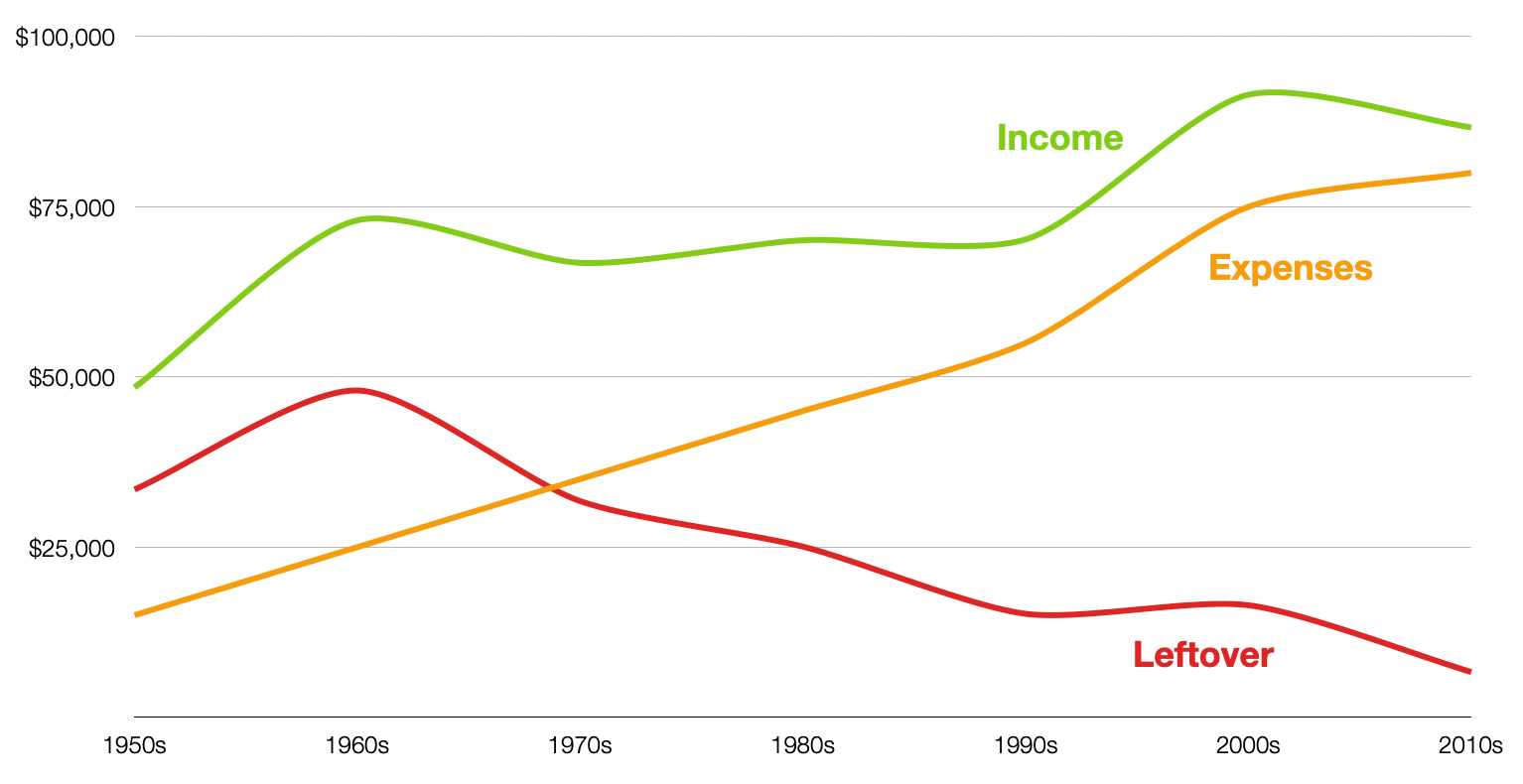

Okay, let’s pivot and take a look at how dramatically finances have changed for average Americans since “trickle down” came along in 1986.

| Decade | Median Income |

Cost of Living Index |

Income Adjusted for 2024 Dollars |

Essential Expenses |

Leftover Income |

|---|---|---|---|---|---|

| 1950s | $4,000 | 26.0 | $48,462 | $15,000 | $33,462 |

| 1960s | $7,000 | 30.2 | $73,013 | $25,000 | $48,013 |

| 1970s | $11,000 | 51.9 | $66,763 | $35,000 | $31,763 |

| 1980s | $20,000 | 89.9 | $70,078 | $45,000 | $25,078 |

| 1990s | $30,000 | 134.6 | $70,208 | $55,000 | $15,208 |

| 2000s | $50,000 | 172.2 | $91,463 | $75,000 | $16,463 |

| 2010s | $60,000 | 218.1 | $86,657 | $80,000 | $6,657 |

Here’s what we did: we started with the median income that families earned in each decade and adjusted it for inflation and the cost of living. Then we factored in essential expenses (think housing, healthcare, and education) to see how much leftover income families had.

Here's the key info in chart form:

What we found is kinda wild:

So, let's just recap. In the 1950s: $33,000 left over. By the 2010s: only $6,000.

This is seriously disturbing: families are working harder and earning more on paper, but somehow, they’ve got less wiggle room than ever. This is all kinds of wrong.

Welcome to the magical world of U.S. tax brackets: a system so thrilling it’s rumored to have been the inspiration for bedtime stories that put accountants’ kids to sleep.

| Bracket | Who's in this bracket | Income Range | Tax Rate | Population |

|---|---|---|---|---|

| 1 | Hustling to Get By | under $11,000 | 10% | 43M |

| 2 | Scraping Through | $11,000 – $47,000 | 12% | 38M |

| 3 | Steady but Careful | $47,000 – $100,000 | 22% | 33M |

| 4 | Comfortably Climbing | $100,000 – $191,000 | 24% | 24M |

| 5 | Starting to Splurge | $191,000 – $243,000 | 32% | 8M |

| 6 | High Earners, Big Plans | $243,000 – $609,000 | 35% | 5M |

| 7 | Running the Show | over $609,000 | 37% | 2M |

From struggling workers to the ultra-wealthy, everyone fits somewhere.

Struggling to make ends meet: students, gig workers, and part-timers often in transitional or precarious work

Examples: part-time cashier ($8k/year), seasonal farmworker ($10k/year)

Living paycheck-to-paycheck, but managing: service workers, junior tradespeople, and freelancers

Examples: full-time barista ($25k/year), admin assistant ($40k/year)

On solid footing, but still keeping an eye on the budget: teachers, nurses, and skilled tradespeople

Examples: teacher ($60k/year), electrician ($85k/year)

Comfortable suburban life: engineers, project managers, medical pros, or small business owners

Examples: pharmacist ($125k/year), tech product manager ($150k/year)

Living well with a touch of luxury: lawyers, senior consultants, and entrepreneurs

Examples: corporate lawyer ($220k/year), radiologist ($240k/year)

Affluent and focused on growing their wealth: surgeons, corporate executives, and franchise owners

Examples: neurosurgeon ($500k/year), corporate VP ($450k/year)

The ultra-rich shaping the world: CEOs, tech founders, and hedge fund managers

Examples: Fortune 500 CEO ($10M/year), hedge fund manager ($5M/year)

Generally, your income determines how much you owe in taxes. The brackets start low and climb higher the more you earn. Pretty easy, right?

But wait! There’s this exasperating hidden gotcha that nobody explains: like many people, I thought you just find your salary on the chart and that’s your tax rate. Wrong. (But more on that in a moment.)

Let’s get one thing straight: there’s no magic formula behind the tax rates or the income brackets we’re using today. They weren’t handed down on stone tablets or dictated by some universal economic truth. Nope. They’re a messy mix of political bargaining that, surprise surprise, tends to favor the wealthy. And political inertia where nobody has stepped back to ask, “Wait, does this even make sense anymore?”

A few years ago, I got a job offer for $195,000, a huge deal for me. I grew up in a paycheck-to-paycheck household, watching my parents struggle to pay bills. I was the first in my family to graduate college, and for most of my life, I watched my bank account like a hawk. So yeah, $195k felt like winning the lottery.

Then I looked up tax brackets and had a full-blown oh shit moment.

At $195k, I’d be in the 32% tax bracket. At $190k, I’d be in the 24% bracket. My brain short-circuited:

What?! Cue the panic: “Am I actually going to make LESS money by earning MORE? What kind of broken system is this?” I was so freaked out, I almost asked them to change the offer to be for less money. Yep, I went full potato on that one.

Thankfully, I did some research and learned the truth. Tax brackets don’t work the way I thought. The higher tax rate only applies to the portion of your income that falls into that bracket, not your entire income. And that’s when I had what I like to call my Cookie Epiphany.

Imagine your income as a stack of 60 cookies, and the government wants some to share with everyone else. But they don’t take the same number from every part of the stack:

So you have 46 cookies left, and you paid 14 in taxes. But notice, they didn’t take 30% of your whole stack, just from the last stack. Swap cookies for cash, and that’s basically how tax brackets work.

Now let’s break it down with real dough. Say you make $60,000. Here’s how your taxes would look under the 2024 brackets for a single person:

Total tax? $8,280. Even though part of your income falls into the 22% bracket, you’re not paying 22% on the whole $60k, just on the top portion.

So no, you don’t make less by earning more. And that’s how I stopped freaking out, accepted the job offer, and learned to make peace with sharing my cookies.

Alright, we're finally done with all the boring stuff leading up to the main event. Thanks for sticking with me. Isn't this fun, all this talk about taxes? 🫠

So here’s the idea: What if we took a page from the past, when paychecks stretched further and the wealthiest among us contributed a bit more to the common good? It’s not about punishment; it’s about generosity and balance. Those with the most resources can afford to lend a hand. And in doing so, they help create a stronger, better-supported society for everyone. That’s not just fair, it’s pretty damn magnanimous.

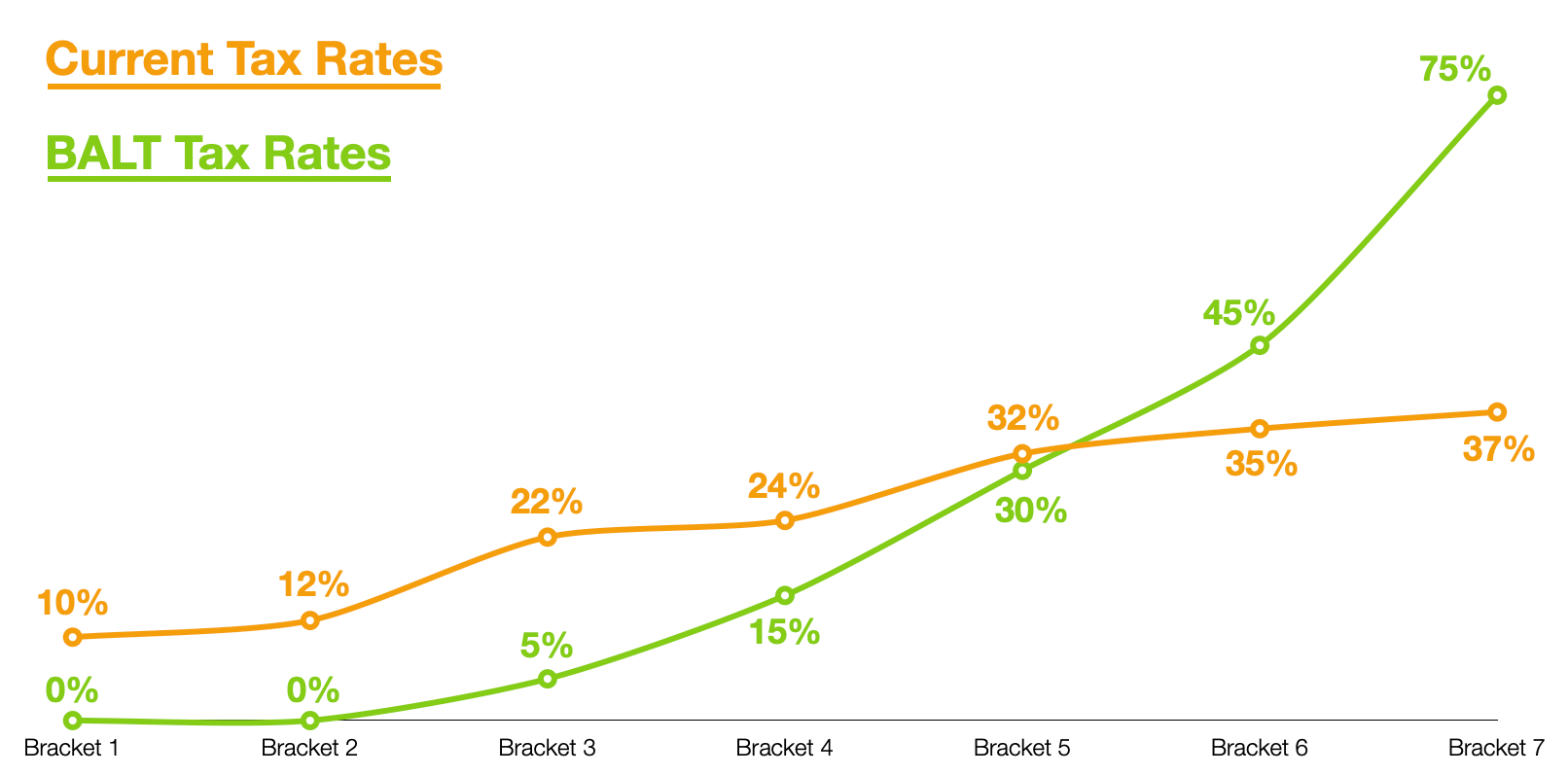

Here’s how the “Build a Longer Table” plan would shake out:

| Bracket | Income Bracket | Current Tax Rate |

Revenue (billions) |

BALT Tax Rate |

Revenue (billions) |

|---|---|---|---|---|---|

| 1 | under $11,000 | 10% | $25 | 0% | $0 |

| 2 | $11,000 – $47,000 | 12% | $216 | 0% | $0 |

| 3 | $47,000 – $100,000 | 22% | $495 | 5% | $113 |

| 4 | $100,000 – $191,000 | 24% | $720 | 15% | $450 |

| 5 | $191,000 – $243,000 | 32% | $704 | 30% | $660 |

| 6 | $243,000 – $609,000 | 35% | $700 | 45% | $900 |

| 7 | over $609,000 | 37% | $925 | 75% | $1,875 |

| Total | $3,785 | $3,998 |

| Income Level | Current Taxes | Takehome | BALT Taxes | Takehome | Difference |

|---|---|---|---|---|---|

| $47,000 | $5,647 | $41,353 | $0 | $47,000 | +$5,647 |

| $100,000 | $17,399 | $82,601 | $2,499 | $97,501 | +$14,900 |

| $240,000 | $55,893 | $184,107 | $31,554 | $208,446 | +$24,339 |

| $500,000 | $146,893 | $353,107 | $147,095 | $352,905 | -$202 |

| $1,000,000 | $330,330 | $669,670 | $489,289 | $510,711 | -$158,959 |

| $10,000,000 | $3,660,330 | $6,339,670 | $7,239,289 | $2,760,711 | -$3,578,959 |

Here’s the sneaky genius of this plan: It benefits everybody, even the wealthy.

That means the guy making $10 million a year is still paying less on his first $240k than he does now. The higher rates only hit the new money above that line.

Because, remember: this is how the “cookie” tax system works. The official name is “progressive taxation”, but I like cookies better.

Any big change like this needs a practical roadmap. Here’s how we’d actually pull this off:

Nothing here is rocket science, just common sense adjustments to make sure the plan works for real people in the real world.

When you understand how tax brackets work, this plan is a win for all of us. More relief for the people who need it most, and a fairer system for everyone else. And yeah, the wealthy pay more, but guess what? They are the strongest among us.

Best of all, these new tax brackets actually generate more revenue than the current structure, ensuring we can fund schools, social programs, and maybe even fix that giant pothole on your street, all while putting more money in the hands of everyday Americans.

And here’s the really cool part: when lower- and middle-class folks have more cash, they actually spend it on things like groceries, clothes, or fixing that leaky roof. That’s pumping money right back into the economy. Compare that to the wealthy, who stash their extra tax savings in investments that mostly benefit, you guessed it, other rich people.

Turns out, giving everyday folks more buying power isn’t just fair, it’s great for business.

Let’s clear one thing up, because I’ve heard some weird notions about the idea of raising taxes on the wealthy. Here’s the truth:

So no, nobody’s raiding anyone’s bank account or swooping in to seize their stuff. Wealthy folks aren’t losing what they already have, just sharing a bit more of the new pie they’re baking.

Seems fair, doesn’t it?

It's not just about numbers on a spreadsheet. It’s about getting real relief to the people who are struggling the most. And the best part? The messaging is so simple even a campaign ad wouldn’t screw it up:

This is the kind of clear, no-BS message that actually resonates with people, especially the RUBIs who are notoriously inattentive.

If Democrats are looking for ideas that will actually land with voters, a plan like this could be a massive game-changer. It’s fair, it’s easy to understand, and it speaks to what people care about most: having more financial security, so they can breathe easier.

Look, I know what some of you might be thinking: “Yeah, yeah, this is just changing the tax brackets. Big whoop. It’s nothing revolutionary.” And you’re not wrong. This isn’t some galaxy-brain, earth-shattering idea. But sometimes, the simplest, most obvious solutions sitting right in front of us are the best ones.

And here’s the deal: the current system is lopsided. It’s squeezing the people who can least afford it while missing the opportunity to have the wealthiest among us lend a helping hand and strengthen the economy for everyone. What we’re talking about here isn’t rocket science. It’s just rebalancing things to make them more reasonable.

BTW, let’s be totally upfront about something: the moment we propose this plan, Republicans will lose their fucking minds. They’ll break out their dumbshit “communism stamp” and start screaming about the apocalypse, say that freedom is dying, and whatever other fear-mongering bullshit they can muster. I can already see the Fox News graphics now, it’s all so tedious and predictable.

But here’s the thing: fuck those guys.

This plan isn’t for the pearl-clutching Republicans who think any tax on the wealthy is one step away from gulags and bread lines. It’s not for the Ayn Rand fan club or the “my third yacht might be at risk” crowd. It’s for the mom working two jobs who can’t afford childcare, the young couple drowning in student debt while trying to save for a house, and the millions of Americans who are one unexpected bill away from disaster.

These people are suffering. They don’t care about ideological purity tests. They only care about being able to breathe a little easier at the end of each month. As Democrats, we need to grow a backbone and stop worrying about what knuckle-dragging troglodytes like Tucker Carlson might say. Let’s have the courage to fight for policies that actually help regular people, even when the wealthy and powerful push back. Because if we don’t, who will?

Democrats, it’s time we picked a fucking side. Are we with the corrupt, freedom-hating, billionaire-slobbering, pick-me crowd? Or are we on the side of those that are suffering and desperately need our help. To me, the answer is obvious, and it’s time we do something about it.

And hey, if you’ve got an economics degree and want to poke holes in this plan and point out that I rounded numbers and approximated shit, be my guest. Tear it apart. Challenge it. Go wild. But don’t lose sight of the bigger picture: this is about fixing a broken system and creating a tax structure that actually works for the majority of people, not just the privileged few.

At its core, the “Build a Longer Table” tax plan is about fairness, stability, and shared prosperity. It’s about making sure everyone has a seat at the table, a meal on their plate, and a fair shot at the opportunities we all deserve.

And if we can achieve that? Then we all win.

Next episode

Get episode updates via email

We'll never share your email, period. We only hit your inbox to announce a new episode, and if you ever want out, unsubscribing is one click. Easy peasy.